Introduction

As a Cuban-American attorney with personal connections to immigration stories, I understand the dream of a secure life in the United States – and the complicated realities that come with it. I’ve seen wealthy clients hesitate to seek U.S. residency because of one major deterrent: taxes. The moment you become a U.S. permanent resident (green card holder), the IRS treats you like a U.S. citizen for tax purposes, taxing your worldwide income (Topic no. 851, Resident and nonresident aliens | Internal Revenue Service). In my Miami practice, I’ve advised global entrepreneurs, from Latin America to Europe and Asia, who told me, “We’d love a foothold in America, but we can’t expose our entire global fortune to U.S. taxes.” And I didn’t blame them – historically, a standard Green Card or EB-5 investor visa meant signing up for IRS taxation on every penny you earn worldwide (Should US citizenship cost $5m?).

That’s why I was astonished and excited when news broke about a new program called the “Gold Card” Green Card. This isn’t your typical visa – it’s a game-changing U.S. residency program specifically designed for ultra-high-net-worth individuals. The headline benefit sounded almost too good to be true: Gold Card holders will not be subject to U.S. taxes on their foreign income (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Yes, you read that correctly. The Gold Card is the only U.S. green card that officially exempts your foreign income from U.S. taxation – a benefit no other American citizen or green card holder gets (Trump’s proposed ‘gold card’ visa comes with a hidden tax break for the wealthy | Robert Frank).

When I first heard this, I nearly fell out of my chair. A U.S. residency with a built-in foreign income tax exemption? For estate planning and tax-conscious clients, that’s the holy grail. I immediately thought of all the global families I’ve worked with: this Gold Card Green Card could be the solution they’ve been waiting for. It promises the freedom and security of U.S. permanent residency without the usual tax nightmare. In this article, I’ll break down how the Gold Card works, why it’s such a revolutionary policy for wealthy international families, and how it stacks up against the standard Green Card and EB-5 visa.

(Spoiler: The Gold Card is in a league of its own – and I’ll explain why, with verified facts and sources.)

Illustrative Example: Don Carlos

Let’s paint a picture. Imagine Don Carlos, a 68-year-old billionaire from Mexico (it could just as easily be an entrepreneur from India, China, the Middle East or anywhere). Don Carlos built a global empire with businesses and investments spanning multiple countries. He has homes in Europe, a portfolio in Asia, and a large family he wants to protect. For years, he’s considered moving his wife, children, and grandchildren to the United States for better security and a stable future. But every time he weighed the move, his advisors warned: a normal U.S. green card will make you a U.S. tax resident. That means yearly filings to the IRS on every dollar you earn worldwide, from foreign stock dividends to overseas real estate income (Topic no. 851, Resident and nonresident aliens | Internal Revenue Service). Plus, as a U.S. resident, his estate could become subject to U.S. estate taxes on global assets – a potential hit to the legacy he plans to leave his kids. The result? Don Carlos stayed put, or looked at other countries’ “golden visa” programs, always keeping the U.S. at arm’s length despite its allure.

Now enter the Gold Card Green Card. It’s 2025, and Don Carlos hears through CNBC and financial advisors that the U.S. has introduced a $5 million investor Green Card – steep in price, but with an unprecedented perk: no U.S. taxes on foreign income (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Skeptical but intrigued, he digs deeper and learns this isn’t a rumor; it was confirmed at the highest levels. In a recent interview on the All-In Podcast, U.S. Commerce Secretary Howard Lutnick (yes, the same Howard Lutnick who leads Wall Street giant Cantor Fitzgerald) personally affirmed that Gold Card holders will only be taxed on U.S.-sourced income – all their money earned abroad will be untaxed by the IRS (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). This is exactly the assurance Don Carlos has been seeking for years.

Picture the impact on his plans: With a Gold Card, Don Carlos can secure U.S. permanent residency for himself and each family member by paying $5 million per person to the program. That’s a hefty $30 million for a family of six, but for someone of his net worth, it’s a small price for peace of mind and a safe harbor. He knows that if political turmoil erupts or a crisis strikes his home country, his family can immediately relocate to the U.S. “at any time they want” (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard) with the full rights of permanent residents. It’s like buying the world’s most valuable insurance policy: an American Green Card that can be used as needed, without triggering the IRS to tax his overseas fortune.

In the past, Don Carlos’s only route to a U.S. Green Card might have been the EB-5 investor visa, which demands a significant business investment ($800,000 to $1 million) and creation of at least 10 American jobs (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard) – and still no relief from global taxation. He actually considered EB-5 years ago, but balked because even after investing and waiting years, he’d end up with a regular green card and the same worldwide tax burden. Many affluent foreigners have felt the same reluctance about EB-5 for this very reason (Should US citizenship cost $5m?). The Gold Card changes that equation overnight. Now, Don Carlos sees a clear path: for the first time, he can have the best of both worlds – U.S. residency for his family’s security and prestige, and the ability to avoid U.S. taxes on non-U.S. income. For a man like him, the Gold Card isn’t just attractive; it’s a game-changer in how he plans his legacy and wealth preservation.

(In fact, one top U.S. official quipped that if he weren’t already American, he’d buy six Gold Cards – one for himself, his wife, and each of his four children – just to have that option to bring his family “home” to America in a crisis (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). This illustrates exactly how ultra-wealthy families view the program: as essential protection.)

Comprehensive Analysis of the Gold Card Program

Investment Requirements

The Gold Card program allows a foreign national to obtain permanent U.S. residency (“green card” status) in exchange for a $5 million investment directly into the U.S. government (not a business). This price tag makes it one of the most expensive immigrant investor programs in the world. By comparison, the traditional EB-5 visa requires an ~$1 million investment (or $800,000 in certain areas) in a job-creating enterprise (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). President Trump, who introduced this plan, calls the $5M price a “bargain” given what it offers (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard), and indeed the demand seems strong (more on that below).

Tax Benefits and Exemptions

What do you get for $5 million? Green Card privileges and then some. You and your immediate family can live in the United States indefinitely as permanent residents, with the option (but not the obligation) to apply for citizenship down the line (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Crucially, the Gold Card is the only U.S. residency status that comes with an official foreign income tax exemption. Normally, a green card holder must report and pay U.S. tax on all income, whether earned in New York or New Delhi (Topic no. 851, Resident and nonresident aliens | Internal Revenue Service). Not so for Gold Card holders. The program’s architects have confirmed that only U.S.-sourced income will be taxed; any income earned abroad is non-taxable by the IRS for Gold Card residents (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). In other words, a Gold Card holder can keep their offshore businesses, investments, and bank accounts growing tax-free from Uncle Sam’s perspective. This unique carve-out is so significant that it actually represents an exception to the usual U.S. tax code (Experts: Trump’s “Gold Card” Program Hinges on Tax Exemption). It’s a benefit even U.S. citizens don’t enjoy – American citizens and regular green card holders are subject to worldwide taxation, no ifs, ands, or buts. As CNBC’s Wealth Editor Robert Frank put it, the Gold Card’s “hidden tax break” could be worth a fortune to the ultra-wealthy, granting a tax benefit “not available to Americans [or] green card holders” under any other program (Trump’s proposed ‘gold card’ visa comes with a hidden tax break for the wealthy | Robert Frank).

Comparison with Other Immigration Options

Let’s compare:

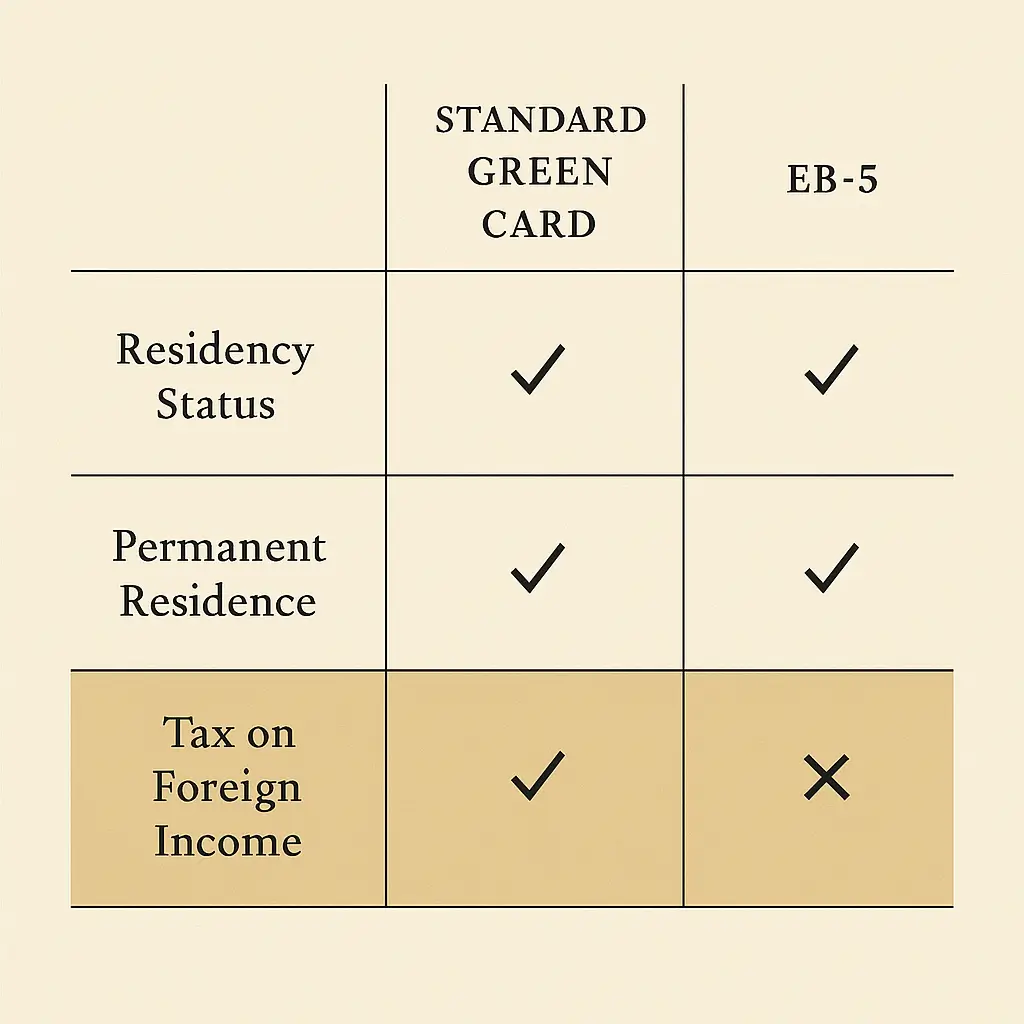

- Standard Green Card (through family or EB-5): Taxed on worldwide income (no exceptions) (Topic no. 851, Resident and nonresident aliens | Internal Revenue Service). Cost: Typically no direct fee (family sponsorship) or ~$1M investment plus 5+ years wait (EB-5). Requirement: If EB-5, must create 10 U.S. jobs and endure a quota backlog (Should US citizenship cost $5m?) (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Result: Permanent resident with all duties (including global tax) and rights.

- EB-5 Investor Visa: Essentially a path to a standard green card by investing in a U.S. business. No tax breaks – once your green card is issued, you’re taxed globally like any resident. Many affluent investors found this route unappealing lately due to the tax issue and long processing times (Should US citizenship cost $5m?).

- Gold Card Green Card: Taxed only on U.S. income; foreign income is exempt (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Cost: $5 million contribution to the U.S. (per person). Requirement: Background checks (“vetting”) for security, but no job creation or business investment needed – it’s a straightforward purchase of permanent residency rights (Lutnick Claims to Have “Sold 1,000” Gold Cards for $5 Billion in One Day – IMI Daily). Result: Permanent resident status, option to pursue citizenship later (though many won’t, since becoming a U.S. citizen would subject them to global tax again (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard)). The Gold Card stands alone as a “green card plus” – it gives all the advantages of U.S. residency (ability to live, work, invest, and send kids to school in the U.S.) while slicing away the biggest disadvantage (worldwide taxation).

Strategic Value for Global Families

From an immigration policy perspective, the Gold Card is revolutionary. The United States has never before offered a tax-incentivized residency like this. Other countries have “golden visas,” but the U.S. combining a direct cash-for-residency program with a tax loophole is new and transformative. This opens the door for ultra-high-net-worth individuals who previously avoided U.S. residency to reconsider. Wealthy magnates from around the world who worry about instability at home can now obtain an American safe haven without the huge tax cost. Howard Lutnick aptly described the Gold Card as a form of “insurance for wealthy families” – a hedge against the unknown (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Pay the fee, secure the card, and keep it in your back pocket. If someday there’s civil unrest, a pandemic, or government seizures abroad, you and your family can be on a plane to the U.S. that same day, knowing you have the right to live here indefinitely with your wealth intact.

Current Program Status and Implementation

Is this all just theory? Not at all. The program is already making waves. In March 2025, Howard Lutnick announced on the All-In Podcast that “yesterday, I sold a thousand” Gold Cards in a single day (Lutnick Claims to Have “Sold 1,000” Gold Cards for $5 Billion in One Day – IMI Daily). This jaw-dropping figure might sound unbelievable, but multiple news outlets have reported it and it demonstrates the pent-up demand among the global elite. (It’s likely these initial “sales” are in principle, pending the formal application launch – which Lutnick said is being built by tech icon Elon Musk and set to go live within weeks (Lutnick Claims to Have “Sold 1,000” Gold Cards for $5 Billion in One Day – IMI Daily).) The key takeaway: wealthy families are already voting with their wallets. They’re eager to seize this opportunity to obtain U.S. residency without the tax downside. And they have good reason to be confident – this policy isn’t a mere campaign promise whispered in the dark. It was publicly declared by the President in a Joint Session of Congress that foreign income would be excluded from taxes for Gold Card holders (Experts: Trump’s “Gold Card” Program Hinges on Tax Exemption), and it’s been openly affirmed by officials like Lutnick who are known for their credibility.

To further highlight the significance, consider that the EB-5 program is capped at under 10,000 visas a year and has long waitlists (14,000+ applicants backlogged, especially from China) (Should US citizenship cost $5m?). It often takes years to get a green card through EB-5, and uncertainty abounds during the process. Gold Card, by design, seems to have no numerical cap announced (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard) – potentially hundreds of thousands could be issued if demand exists. Processing is expected to be faster (the administration signaled it wanted to roll this out “very, very soon” (Experts: Trump’s “Gold Card” Program Hinges on Tax Exemption)). In essence, the Gold Card sidesteps the bottlenecks and red tape that have plagued investor immigration in the past. No wonder immigration attorneys told CNBC they’re already getting flooded with calls from the world’s ultra-wealthy about the Gold Card (Should US citizenship cost $5m?). It’s the hottest ticket in town for those who can afford it.

The U.S. government isn’t doing this out of pure altruism, of course. Gold Card holders can choose to upgrade to U.S. citizenship after a certain number of years (likely five years, as with other green cards), but interestingly, many are expected not to do so (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Why? Because becoming a citizen would end the foreign income exemption – it’s actually more advantageous for them to remain long-term permanent residents under the Gold Card status. This is a reversal of the usual immigrant mindset; the coveted prize here is the green card itself, not necessarily the passport. And that’s fine – the U.S. still gains economically from having these families invested in the country.

In summary, the Gold Card Green Card is a paradigm shift in U.S. immigration policy. It creates a new, elite lane for global investors to become Americans (short of a passport) on terms uniquely favorable to them. By explicitly allowing Gold Card residents to avoid U.S. global taxation, the program removed the number one deal-breaker for wealthy foreign families. This single feature makes the Gold Card the only U.S. residency option of its kind – no other visa or green card, not even marriage or extraordinary talent visas, comes with an IRS hall-pass for foreign income. For international families concerned with estate planning and wealth preservation, the Gold Card offers something truly revolutionary: U.S. residency as a safeguard for your family’s future, without turning your worldwide assets into taxable fodder for the IRS. It’s hard to overstate how important that is if you’re in the shoes of someone like our hypothetical Don Carlos (or any real-life magnate). The ability to enjoy life in Miami or New York, invest in U.S. ventures, have your children attend U.S. universities – all while your overseas earnings remain yours, untaxed – is a benefit that until now was impossible under American law.

Author’s Perspective

I’ll be honest: as an attorney and an immigrant son, I never imagined I’d see the day when the United States offers a green card that lets you legally sidestep the IRS on foreign income. It sounds like fantasy – but it’s now on the books, backed by credible voices and initial results. When I first heard Howard Lutnick describe the Gold Card’s terms, I was cautiously optimistic. Promises in politics come and go. But Lutnick’s word carries weight. This is a man who, after losing 658 employees (and his own brother) on 9/11, vowed to take care of the victims’ families – and he delivered, paying out over $180 million of his firm’s profits to those families over five years (After five years, brokerage fulfills promise to survivors). In short, Howard Lutnick has a track record of keeping his promises and doing the right thing even under the toughest circumstances. So when he confirms that Gold Card holders won’t pay U.S. taxes on non-U.S. income (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard) and even puts his reputation on the line by announcing 1,000 cards sold in a day, I believe him. And the fact that this policy was publicly affirmed by the President in front of Congress (Experts: Trump’s “Gold Card” Program Hinges on Tax Exemption) gives me further confidence that it’s real and moving forward.

From my perspective as a legal advisor, the Gold Card is nothing short of a game-changer for international estate planning and immigration strategy. It finally bridges the gap between the U.S. and global wealth in a way that allows a win-win scenario: families like Don Carlos’s can establish a life in the U.S. and avoid the punitive tax exposure that used to come with that privilege, while the U.S. gains an influx of capital and enterprise. If you are a high-net-worth individual or part of an international family that has held back from U.S. residency due to tax fears, the landscape has fundamentally shifted in your favor. This is a limited club by design (the price tag alone ensures that), but if you have the means, the Gold Card Green Card might be the smartest $5 million investment in your family’s future you’ll ever make. It secures a legacy in the United States, provides a safety net for generations, and crucially, it does so without Uncle Sam laying claim to your worldwide earnings.

Conclusion

The Gold Card Green Card is the only U.S. residency option that lets you avoid global taxation (Trump’s proposed ‘gold card’ visa comes with a hidden tax break for the wealthy | Robert Frank). For wealthy foreigners who value U.S. stability but shunned U.S. taxes, this is your moment. The program is real, it’s happening now, and it’s backed by people who mean business. If you’ve ever dreamed of calling America your “backup home” or gifting your heirs the option of an American life – without burdening them with U.S. worldwide taxes – the Gold Card makes that possible.

Services and Disclaimer

I’m Attorney J.O. Valentino, and my firm offers personalized consultations to map out strategies for U.S. residency through investment, trust and estate structuring, and tax minimization. Given the novelty of the Gold Card, getting expert advice is crucial to navigate the legal fine print and make the most of this opportunity. Contact me today to schedule a private consultation – let’s ensure that if you invest in a Gold Card, it truly becomes a golden foundation for your family’s future.

Disclaimer: This article is for informational purposes only and not formal legal or tax advice. U.S. immigration policies and tax laws are complex and evolving. The Gold Card program is new (as of 2025), and while sources confirm its key features as of now, details could change with legislation or regulatory guidance. Always consult with a qualified attorney and financial advisor about your specific situation before making decisions. J.O. Valentino Law PLLC can assist by working in tandem with immigration counsel and tax professionals to provide a comprehensive plan tailored to you. We are based in Miami, Florida, but serve ultra-high-net-worth clients globally. Our services include international estate planning, asset protection, cross-border tax planning, and now, guidance on leveraging the Gold Card Green Card to achieve your family’s goals.

Your legacy deserves nothing less than the best opportunities – and it’s my honor to help you seize them.

Sources

- CNBC – Trump ‘Gold Card’ Visa’s Hidden Tax Break (Robert Frank’s Inside Wealth newsletter) – Gold Card offers a tax benefit not available to Americans or other green card holders (Trump’s proposed ‘gold card’ visa comes with a hidden tax break for the wealthy | Robert Frank).

- WealthManagement.com – Experts: Trump’s ‘Gold Card’ Hinges on Tax Exemption – Trump’s proposal would exclude foreign income from U.S. taxes, an exception to the U.S. tax code (Experts: Trump’s “Gold Card” Program Hinges on Tax Exemption); Advisors say an exemption is essential for uber-wealthy to consider U.S. residency.

- Business Standard – 1,000 Gold Cards Sold, $5B Raised in One Day – Commerce Sec. Howard Lutnick confirms Gold Card holders can live in the U.S. indefinitely without paying tax on foreign income; only U.S.-earned income is taxable (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard). Also, Lutnick calls the Gold Card an “insurance policy” and notes he’d buy one for each family member if he weren’t American.

- Morning Brew – Should U.S. Citizenship Cost $5M? – Many affluent foreigners are reluctant to use EB-5 visas because green card holders must pay taxes on overseas income (unlike Gold Card holders) (Should US citizenship cost $5m?).

- IRS Topic No. 851 – U.S. Resident Aliens (green card holders) are taxed on worldwide income, just like U.S. citizens – no foreign income exclusion for standard green cards (Topic no. 851, Resident and nonresident aliens | Internal Revenue Service).

- Chron (AP News) – After 9/11, Lutnick Fulfilled Promise – Cantor Fitzgerald CEO Howard Lutnick delivered $180 million (25% of profits over 5 years) to 658 victims’ families, honoring his word (After five years, brokerage fulfills promise to survivors).

- IMI Daily – Lutnick on All-In Podcast – Lutnick claims 1,000 Gold Cards sold in one day; explains the program replaces EB-5 and allows avoiding worldwide tax by remaining a permanent resident (optional citizenship) (Lutnick Claims to Have “Sold 1,000” Gold Cards for $5 Billion in One Day – IMI Daily).

- Business Standard – Trump’s Gold Card to Replace EB-5 – Gold Card grants permanent residency without EB-5’s job creation requirement, costs $5M each; no cap announced (1,000 Trump gold cards sold in a day, each worth $5 million: US officials | Personal Finance – Business Standard).

Call: (305) 634-7790

Email: JO@JOValentino.com

Contact: JOValentino.com/contact

Share: