Capital gains step up basis can mean millions in tax savings if leveraged correctly — yet Val Kilmer’s heirs missed out because he sold his beloved Santa Fe ranch before death. As an attorney who witnessed the devastation of a mismanaged estate after my grandfather’s passing, I’m passionate about ensuring families don’t lose wealth unnecessarily. Read my story here: About me.

Val Kilmer’s Santa Fe Estate Sale: Capital Gains Consequences

Val Kilmer, the beloved actor known for his roles in Top Gun and Batman Forever, passed away at 65, having battled throat cancer for over a decade. He spent two peaceful decades living on a ranch in Santa Fe, New Mexico—land he deeply cherished. But in 2011, he sold it for approximately $33 million. That decision, while personal, came with a steep tax consequence his children will never recover from. It’s a classic example of how misunderstanding the capital gains step up basis can lead to avoidable tax losses.

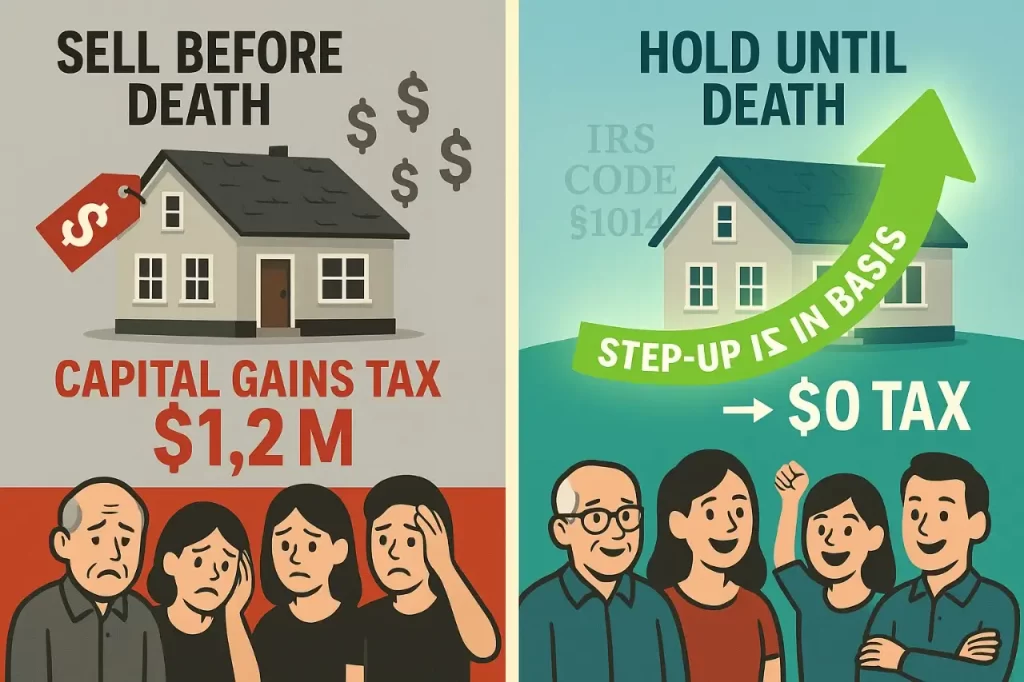

Had Kilmer held onto the ranch until his death, his heirs would have received what’s called a step-up in basis. Instead, by selling it during his lifetime, Kilmer triggered a massive capital gains tax bill.

Understanding the IRS Capital Gains Step Up Basis

When someone dies, the IRS allows their heirs to receive inherited property at its current market value—not the original purchase price. This is known as the step-up in basis. The capital gains step up basis is one of the most powerful yet underused estate planning tools available to families with appreciated assets.

For example:

- If someone buys a ranch for $1 million and it’s worth $10 million at their death,

- The heirs inherit it at a $10 million basis.

- If they sell it for $10 million, they owe no capital gains tax.

This legal mechanism saves families millions of dollars—money that would otherwise be paid to the IRS. But it only works if the property is owned at death. Sell too soon, and the gain becomes taxable.

How to Eliminate Capital Gains with a Step‑Up Strategy

Capital gains tax applies when you sell an asset for more than you paid for it. For high-value property like Kilmer’s ranch, those taxes can be staggering.

By holding assets until death:

- You eliminate decades of appreciation from taxation.

- Your heirs can sell immediately and pay nothing in capital gains.

- It’s one of the most effective estate planning tools available to families with real estate.

Kilmer’s decision to sell before death cost his estate dearly. Unfortunately, this is one of the most common estate planning mistakes made by people who believe they’re simplifying things for their heirs. What they’re really doing is creating a silent, avoidable tax bill—one that I help my clients prevent through strategic planning every day. With proper planning, the capital gains step up basis can be the difference between a preserved inheritance and a six-figure tax bill.

Example: South Florida Commercial Property Plan

Father owned a commercial building in South Florida he purchased in the 1980s for $400,000. Over time, the property appreciated to $5.4 million. Before he passed, Father considered selling to simplify things for his Daughter.

But his Banker advised him to speak with an estate attorney. After meeting with me, we decided to transfer the property into his revocable trust and hold it through the remainder of his life.

When Father passed, Daughter inherited the building at the stepped-up basis of $5.4 million. When she sold it months later, she owed zero in capital gains tax. Had Father sold it during his lifetime, he would have paid nearly $1.2 million in capital gains.

Breakdown: IRS Code §1014 and Estate Planning

Under IRS Code §1014, the step-up in basis allows beneficiaries to reset the cost basis of inherited property to its fair market value at the date of death. This applies to:

- Real estate

- Stocks

- Business interests

- Collectibles

All of these can qualify for the capital gains step up basis if held until death and passed to heirs. If the asset is sold during the owner’s life, capital gains are calculated from the original purchase price, and taxes must be paid. But if it’s passed down after death, those gains are wiped away.

In Kilmer’s case, by selling during his lifetime, he:

- Triggered federal capital gains taxes

- Lost a unique opportunity to pass tax-free wealth to his children

- Disrupted the long-term legacy of his ranch

Make Sure Your Voice—and Legacy—Are Heard Legally

Val Kilmer also lost much of his ability to speak during his illness. That’s a painful reminder for all of us: Make sure your voice is heard—legally—before it’s too late.

You can do that with:

- A last will and testament

- A revocable living trust

- Advance healthcare directives

- A durable power of attorney

Whether it’s your words or your wealth, estate planning ensures your intentions live on, even if your voice cannot.

My Estate Planning & Real Estate Experience

Since founding my law firm in 2016, I’ve walked alongside families during their most vulnerable moments—helping them navigate the legal maze after the loss of a loved one. I believe estate planning and probate aren’t just legal processes—they’re acts of love, protection, and legacy.

My team and I handle:

- Wills and Revocable Trusts

- Summary and Formal Administration

- Real Estate Inside Estates

- Asset Protection & Medicaid Planning

- Post-death Tax Strategy

Whether you’re a father protecting your children, a business owner structuring your legacy, or a retiree securing your peace, I tailor each plan to your goals and ensure your wishes are carried out with dignity and clarity.

Books Worth Reading

You can download any of these free resources to help you get started:

- The Essential Guide to Florida Estate Planning

- Star Spangled Planner

- Global Family’s Guide to U.S. Inheritance Law – Gold Card Advantage

- The Florida Realtor’s Guide to Probate Properties

Fun Learning with Celebrity News Videos

Follow me for entertaining, smart videos on estate planning, probate, and inheritance lessons from celebrity cases:

Legal Disclaimer

This article is for informational purposes only and does not create an attorney-client relationship. The only way to create an attorney-client relationship with me is to receive a signed writing from me stating that I am accepting your case.

Wealthy families and international investors need an attorney to provide strategic estate tax planning.

Families suffering expensive long-term-care need an attorney to provide Medicaid crisis planning.

Beneficiaries who inherit a home and see their taxes jump up need an attorney to fight to lower their tax bill.

I write wills, trusts, powers of attorney, and health care surrogates.

If you need letters of administration, I represent you in probate.

Did you have a tough probate? I can appeal it.

Get In Touch

You have three ways to get in touch with me:

- You can call me at (305) 634-7790

- You can email me at JO@JOValentino.com

- You can fill out the contact form at www.JOValentino.com/contact

If you’re not sure whether your current estate plan makes the most of the capital gains step up basis, call my office today to review your options.

FAQs

What is a capital gains step up basis?

It adjusts inherited property’s cost basis to its market value at death, eliminating tax on lifetime gains

Why did Val Kilmer’s heirs lose money?

He sold his Santa Fe ranch during his lifetime, triggering capital gains taxes instead of receiving a stepped‑up basis.

What assets qualify for a step‑up in basis?

Real estate, stocks, business interests, and other capital assets

Can I still benefit from step‑up basis planning?

Yes—holding appreciated assets in a trust until death ensures heirs receive the stepped‑up basis and avoid capital gains.

Share: